July 1st: No More Grace

The regulatory landscape of the cryptocurrency market is undergoing significant changes in 2026 with the transition period stipulated by the MiCA regulation ending on July 1st. If a service provider is not fully compliant with MiCA, it risks having to cease all or part of its crypto services in the EU.

This risk is not theoretical: the end of the transition period will significantly increase the level of oversight and the consequences are already known. Administrative penalties amount to €5,000,000 or 3% of total annual turnover, whichever is higher. By 2026, we can expect a sharper segmentation between players capable of upholding institutional-grade standards and those confined to less demanding jurisdictions.

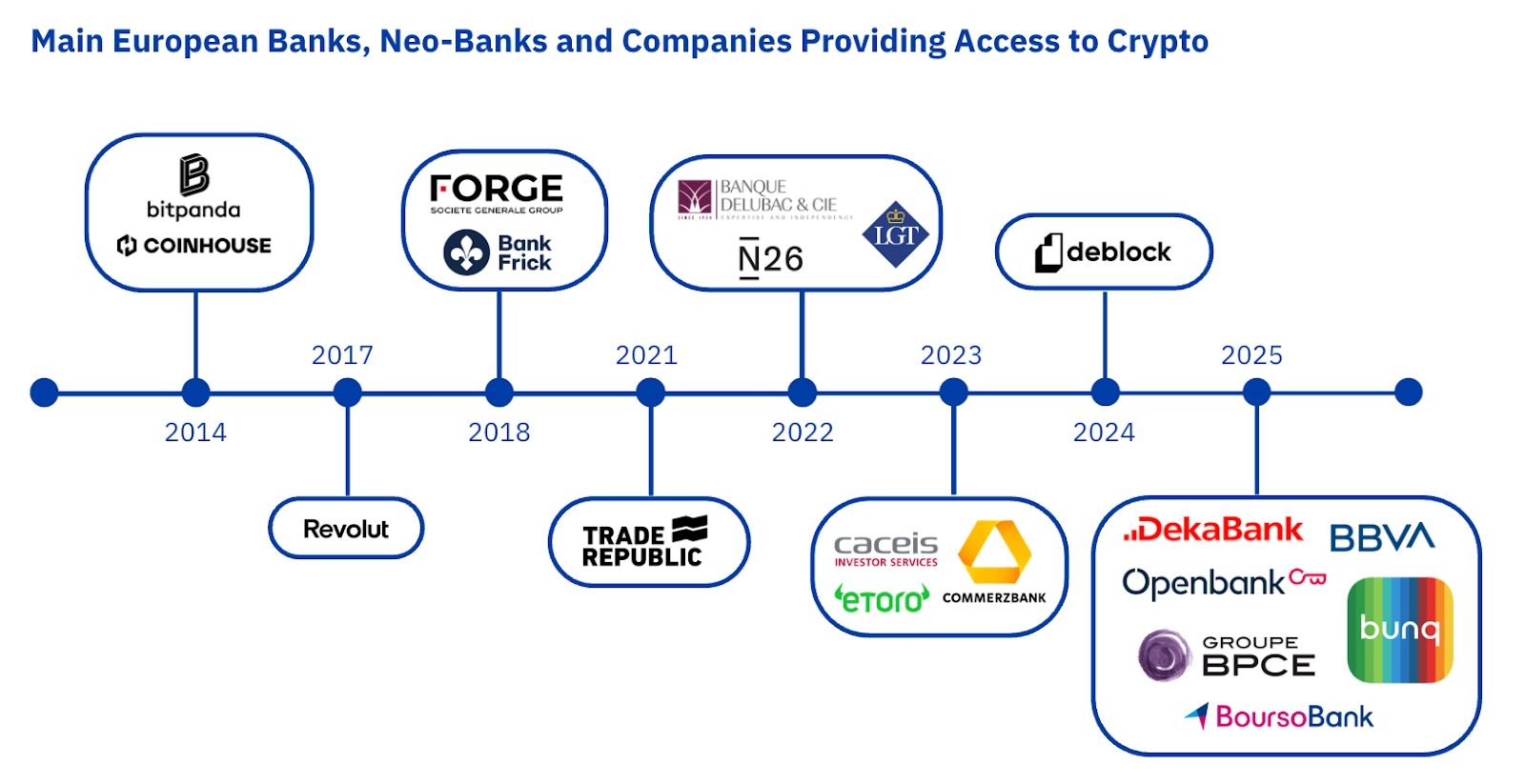

This shift is driven by the market’s rapid expansion. More and more actors are entering the game, which mechanically increases the number of crypto-asset service providers falling within MiCA’s scope. As a result, the regulation framework will extend to a broader set of players across the EU.

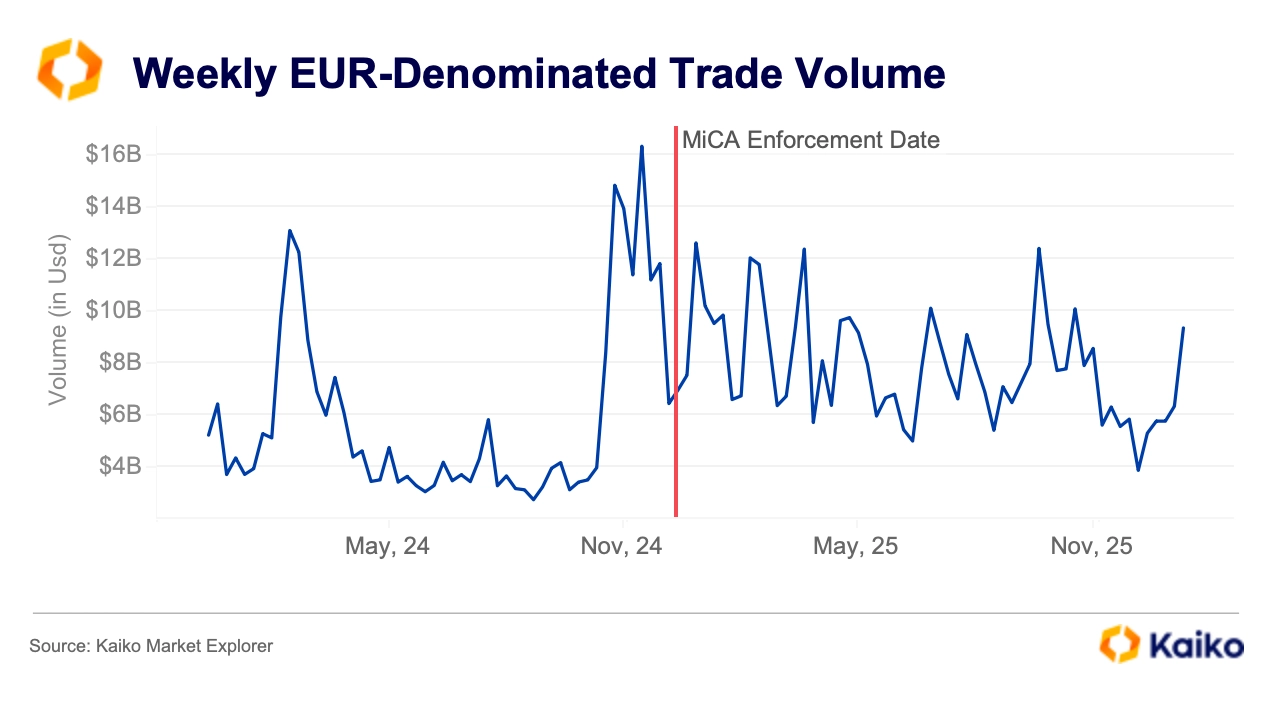

Similar to the number of players, EUR-denominated trade volume is also higher, specifically since the end of 2024.

MiCA does not introduce an exotic regulatory regime for crypto; rather, it largely transposes regulatory logics that are already well established in traditional finance. The same core approach can be found in MiFID II: market entry is regulated, services are framed by clear requirements, conduct-of-business rules are imposed, and transparency and risk management are organized accordingly. In this sense, crypto is being treated as a market segment expected to operate under standards comparable to those of traditional financial markets.

MiFID II has primarily structured the client relationship around transparency and best execution, and MiCA follows the same philosophy. Its positioning is, in fact, structural. Crypto combines often extreme volatility, a risk of rapid losses for retail clients, operational risks, and a cross-border dimension that calls for a coordinated response. In this context, from a European regulatory perspective, the higher the perceived risk, the higher the expected level of investor protection and supervisory control tends to be.

Building on that structural logic, the key point is that these principles are not merely theoretical but they are actively supervised and, when breached, can lead to tangible enforcement actions, best execution being a particularly clear example. The AMF Sanctions Committee, in its decision of August 4, 2021, identified professional shortcomings including the “control of the best execution policy”, and imposed financial penalties of up to €25 million on the company Amundi Asset Management.

Proof Over Promises

As July 1, 2026 approaches, MiCA’s requirements will no longer be an option. As under MiFID II, transparency and best execution will no longer be merely stated principles, but demonstrable obligations. In a fragmented and volatile crypto market, the ability to objectively measure execution quality in a reproducible and auditable way becomes a key criterion for viability. To quote article 78 of MiCA relating to the execution of orders on crypto-assets on behalf of clients, it explicitly stipulates the obligation of best execution and the consideration by the crypto-asset service provider of factors such as price, cost, speed of execution, purpose of execution and settlement, and conditions of securing or holding crypto-assets.

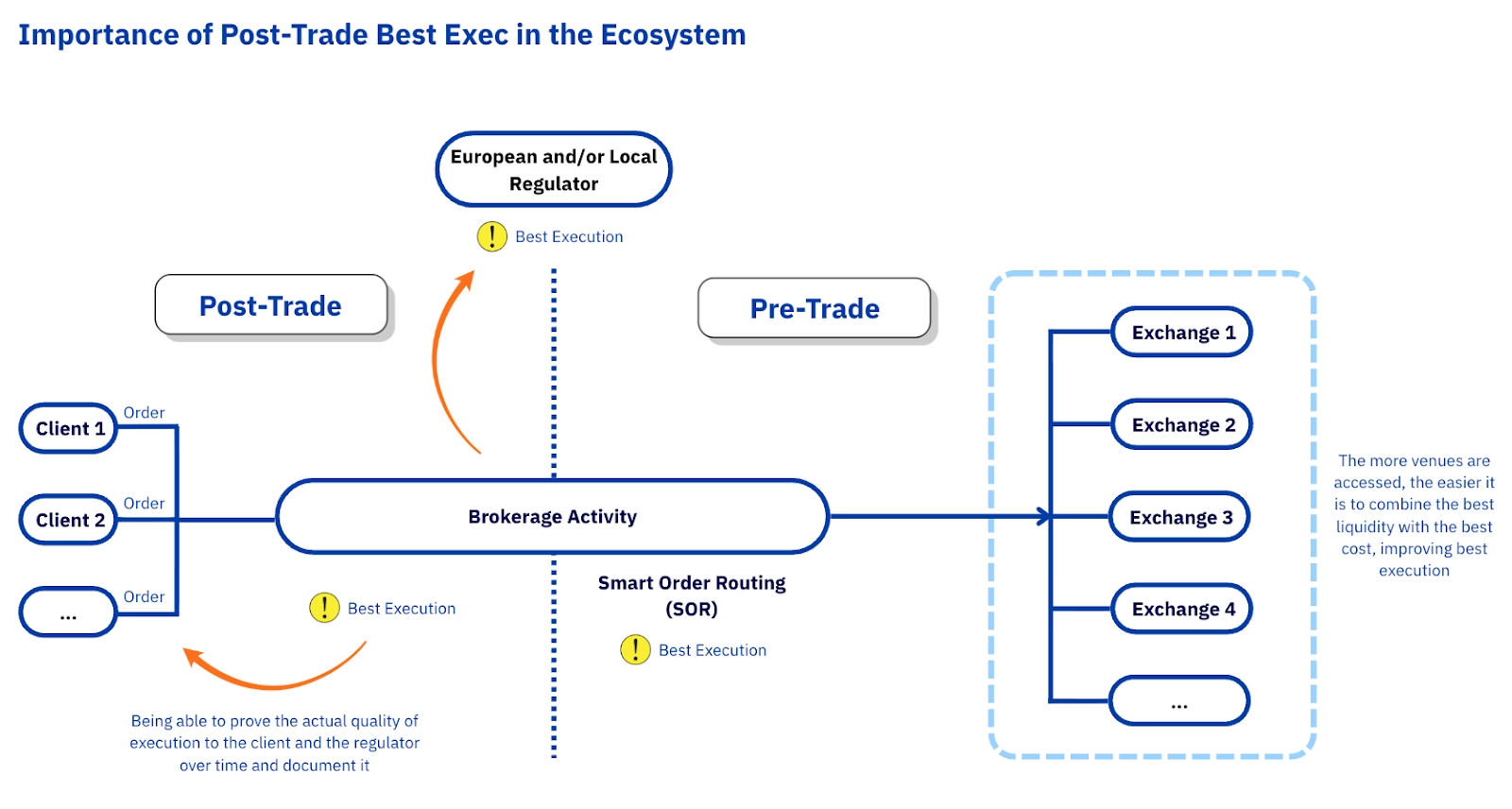

In this context, post-trade capabilities in particular become a core pillar of crypto best execution. Beyond achieving a good price at execution, firms must be able to demonstrate that outcomes were optimal. Robust post-trade analytics and reporting are therefore essential to monitor execution quality over time and demonstrate compliance to clients and regulators.

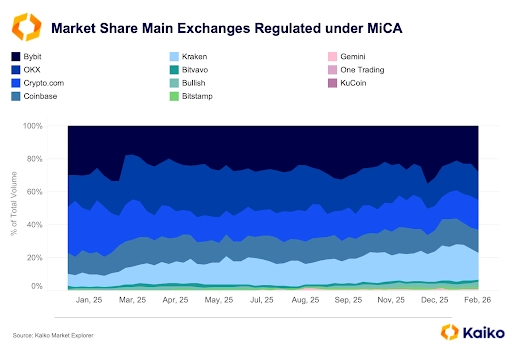

At a global level, price discovery for any given cryptocurrency is fragmented across 100+ exchanges, while in Europe only a defined subset of venues are MiCA-compliant and therefore available for compliant brokers to execute on.

Therefore, proving crypto best execution requires continuous, 24/7 visibility into hundreds of order books and market conditions across all relevant listed markets. It also requires the ability to store and retain this information over time, at a scale that can quickly reach petabytes of data, so firms can demonstrate retrospectively, and to regulators, that they systematically sought and achieved the best available terms. Note that Article 76 of MiCA requires CASPs to maintain these records for at least 5 years. This is why brokerage firms rely on trusted, independent data providers, consistent with the logic of MiCA and aligned with MiFID II’s principles of acting in clients’ best interests and justifying execution policies.

What does Kaiko offer – Best Execution Pricing with L2 Tick-level Data

Designed to meet both MiCA and wider global compliance requirements, Kaiko Best Execution allows you to simulate execution across your selected venues, reconstructing real market conditions at the exact time of your trade, taking into account the order size. Backed by data sourced on all venues you’re executing on, this delivers a trusted, independent, and definitive demonstration of execution quality to regulators and clients.

Additionally, Kaiko also provides a replicable and auditable benchmark, giving you the confidence to justify every trading decision and meet regulatory expectations.

With Kaiko Best Execution, you have a flexible stack where you can design and evidence your company’s policy by:

- Selecting the exact exchanges that align with your best‑execution strategy

- Simulating execution across your selected venues

- Implementing a bespoke methodology (venue filters, weights, controls, order size etc.)

All while maintaining full control of monitoring and audit trails, with access to the raw trades (timestamp, price, volume, side) and full L2 order book used to compute the best execution proof Kaiko provides you with.

In taking this approach, you not only meet MiCAs compliance threshold, but also gain a liability shield that shows you take the regulations seriously. Showcasing to regulators or civil litigators that you work with an independent, market-standard data provider with comprehensive coverage signals that you have taken the steps expected by the legislation, and offers a substantive defence against any challenges raised.

Learn more about how our Best Execution solution can help you meet critical MiCA requirements.

Alternatively, Contact our expert team for a trial today