New research reveals that options on BlackRock’s spot Bitcoin ETF (IBIT) priced tail risk dramatically differently than Deribit’s BTC options for most of 2025, with major implications for cross-venue risk management.

The Bitcoin options market now runs on two parallel tracks, and they are not interchangeable, according to a new market report by MerQube and Kaiko, Measuring Risk in Crypto Options.

The report finds that despite sharing the same underlying asset, the crypto-native Deribit platform and the US-regulated IBIT options market priced risk materially differently across most of 2025. From November 2024 through December 2025, IBIT’s volatility surface exhibited wider swings in skew, the premium for downside protection, and higher convexity on the put wing than Deribit’s BTC options, particularly during periods of institutional onboarding and market stress.

IBIT OI Peaked at $53.3bn, Call-to-Put Ratio Compressed to 1.8:1

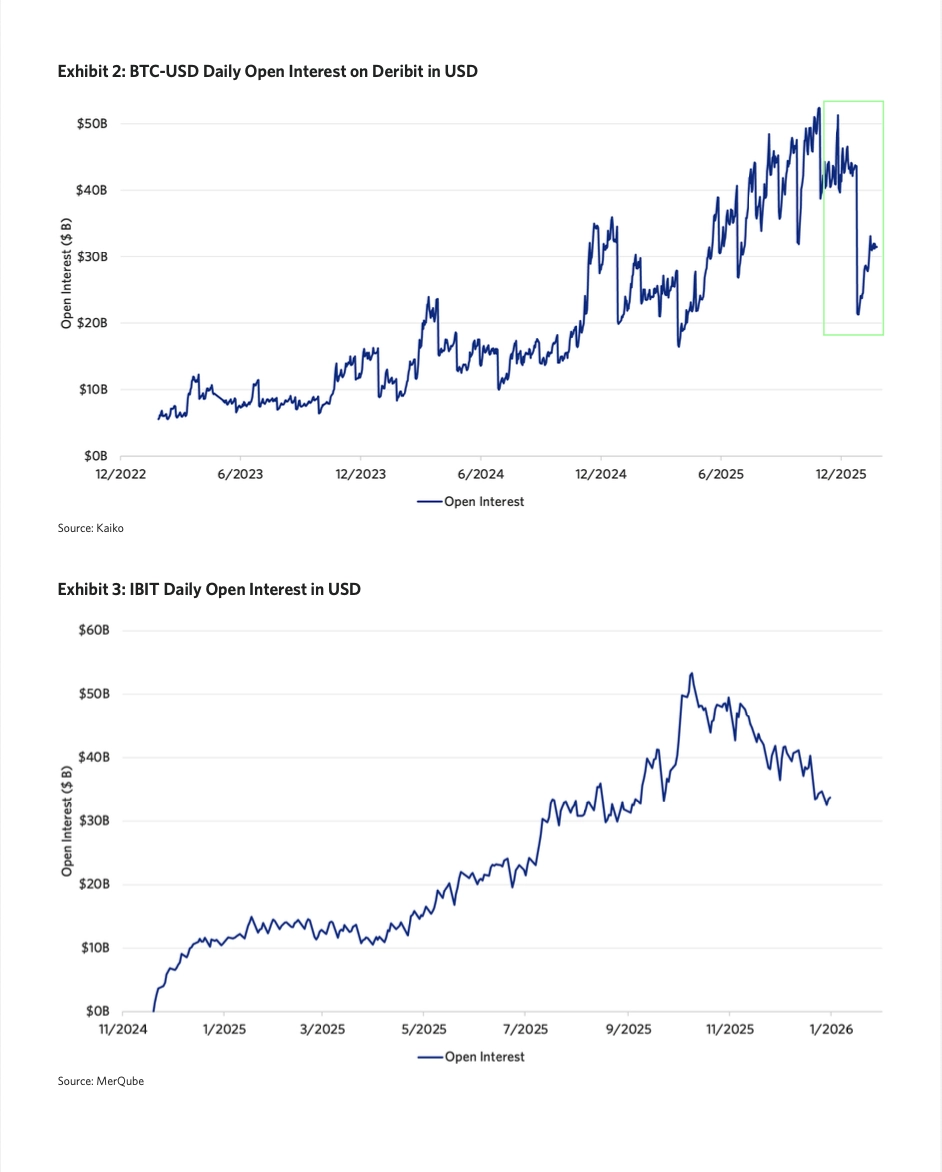

Launched on Cboe in November 2024, options on BlackRock’s iShares Bitcoin Trust (IBIT) saw unprecedented adoption. Open interest crossed $10bn within three weeks, hit $30bn by mid-July 2025, and peaked at $53.3bn (7.8mn contracts) on October 9, 2025 — surpassing the lifetime volume of ProShares’ futures-based BITO ETF in months.

The report highlights that while call interest dominated from day one, the call-to-put ratio compressed from 4.3:1 at launch to 1.8:1 by December 2025, signaling a shift from directional bullish speculation toward hedging and structured product demand. Long-dated open interest ( >16 weeks) routinely accounted for 30–40% of total notional, indicating institutional participation in portfolio insurance and medium-term risk taking.

Key findings from the Kaiko research report

By comparing 1-month implied volatility surfaces for the same monthly expiry, the research identified three distinct phases:

Phase 1 (Nov 2024 – Mar 2025):

IBIT skew ran consistently below Deribit BTC skew, driven by early directional bullish demand (call-to-put ratio above 4:1). On March 3, BTC skew hit 23.5% versus IBIT’s 13.6%, a gap of nearly 10 points.

Phase 2 (Late Mar – Jul 2025):

The relationship inverted sharply. IBIT skew surged above BTC, peaking at 33.4% on July 1 (vs. BTC’s 18.1%), a spread of 15.4 percentage points. IBIT convexity reached 22.5% versus BTC’s 12.0%. This coincided with the SEC raising IBIT position limits from 25,000 to 250,000 contracts and the introduction of cash-settled FLEX options, which drew institutional hedgers who bid up the cost of downside protection.

Phase 3 (Aug – Dec 2025):

Convergence followed. By late September, skew readings were nearly identical (BTC 17.6% vs. IBIT 17.5%). For the December expiry, IBIT skew actually fell below BTC skew, flipping back to a Phase 1-type relationship as market maker capacity expanded and crypto-native investors sought protection on Deribit following the October 10th liquidation cascade.

Read the Report

The full report, Measuring Risk in Crypto Options, is now available.

Read the Full Report

About MerQube

MerQube is an innovative technology provider offering design and calculation solutions for rules-based investment strategies and passive solutions. Launched in 2019 by a team of index industry veterans and technology experts, MerQube was created as a technology-driven answer to the most sophisticated rules-based investment strategies. MerQube now has approximately USD 27 billion in assets tracking its indices. For more information, please visit www.merqube.com.

This article is for informational purposes only and does not constitute a recommendation. None of the content herein should be considered as investment advice or a substitute for it. Investments involve risks. There is a possibility of losing your entire invested capital. This research report was paid for by Bitvavo, but written independently by Kaiko.