Join us for an exclusive webinar with Lise

The Data Behind Tether’s Depeg.

19/06/2023

Welcome to the data blog!

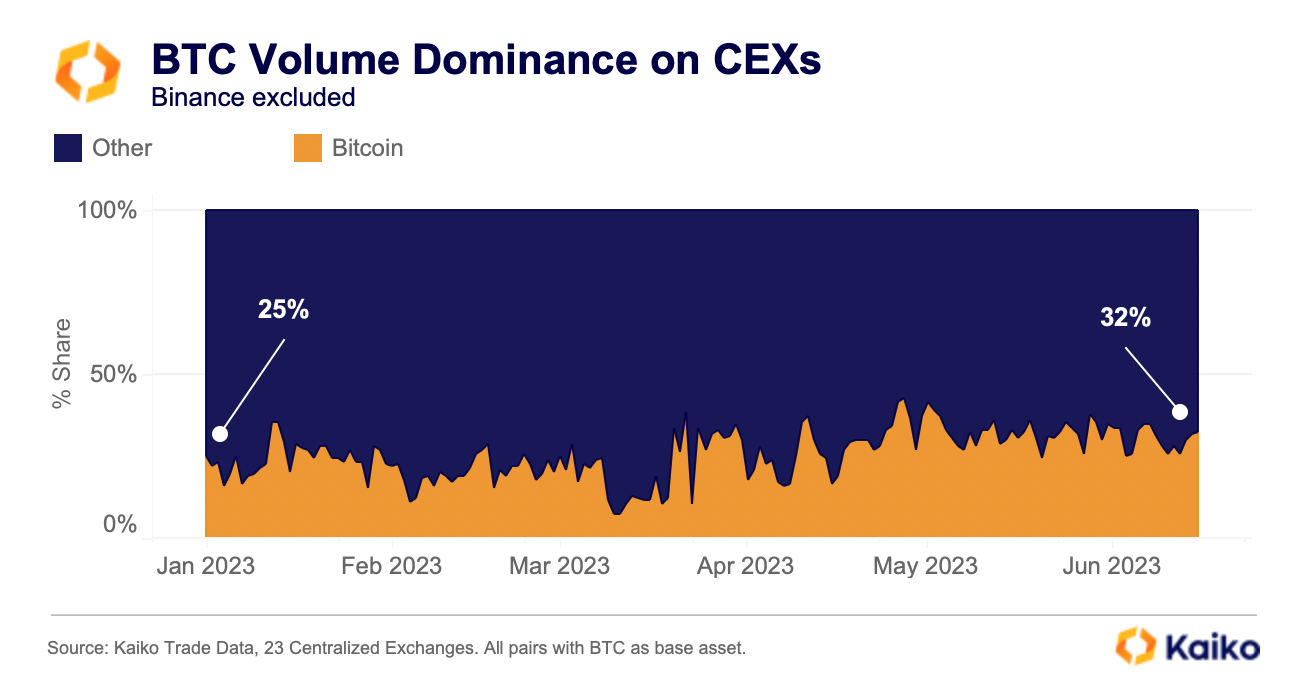

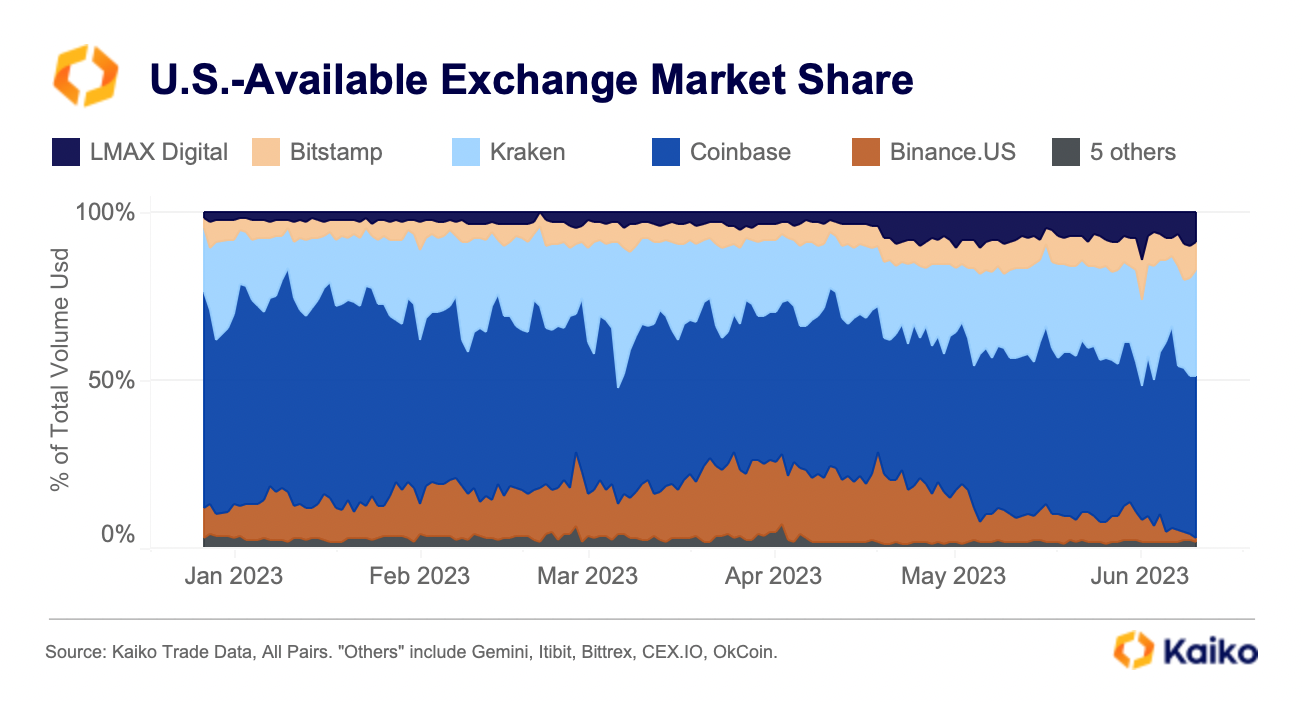

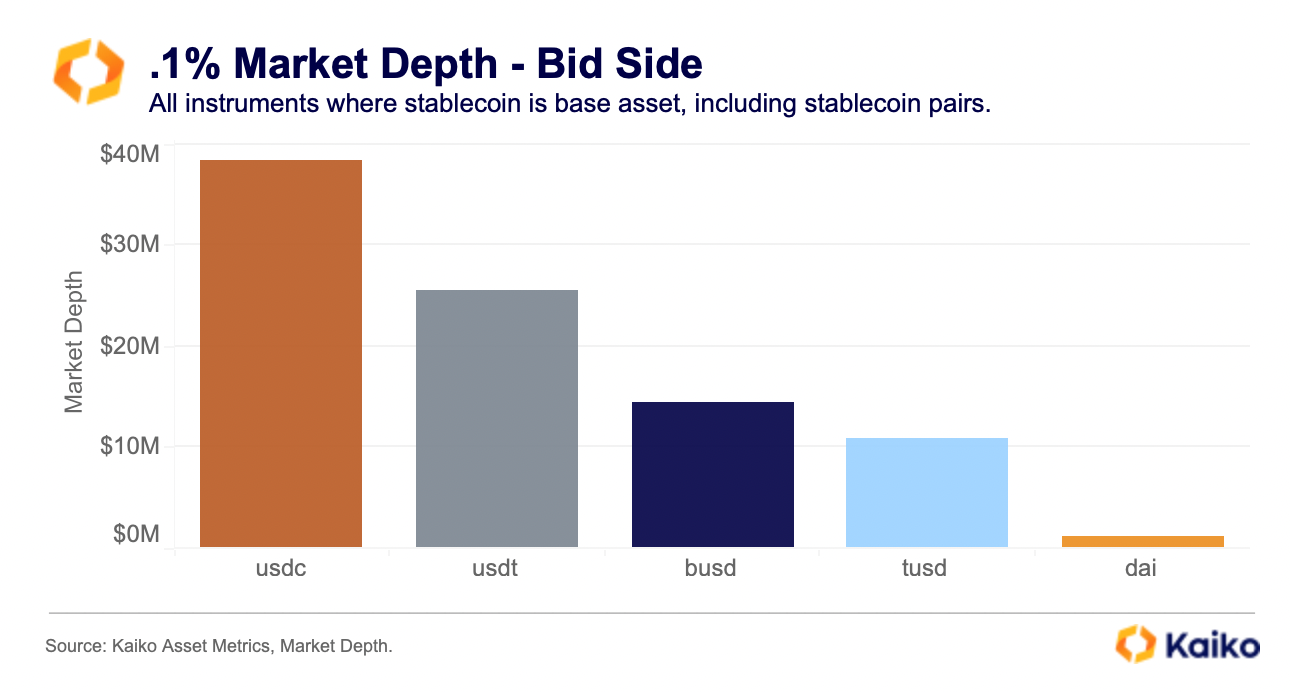

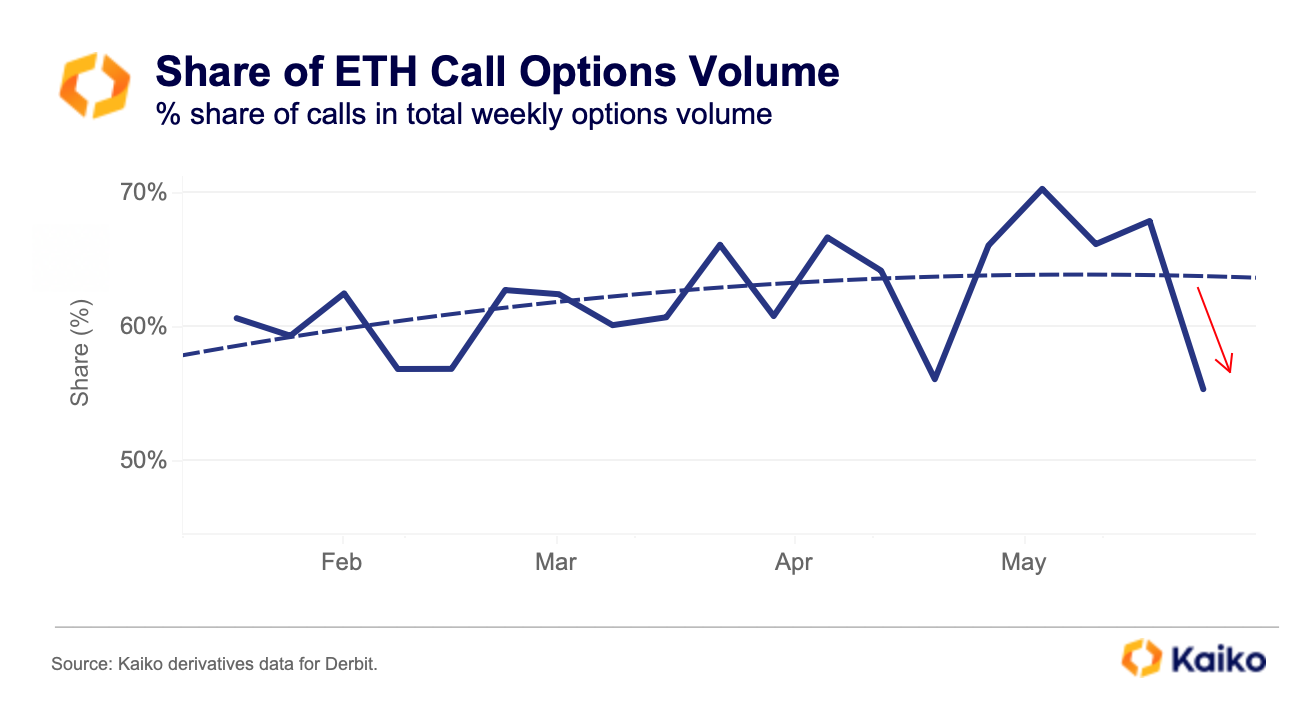

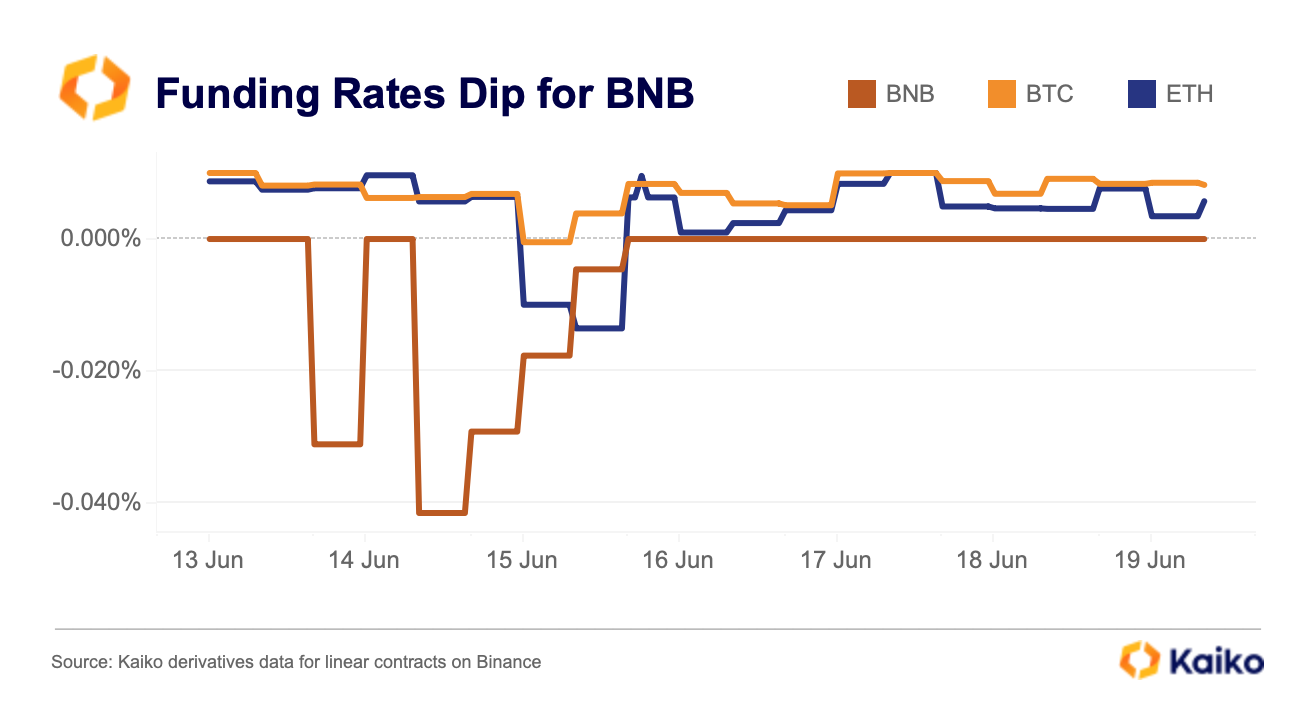

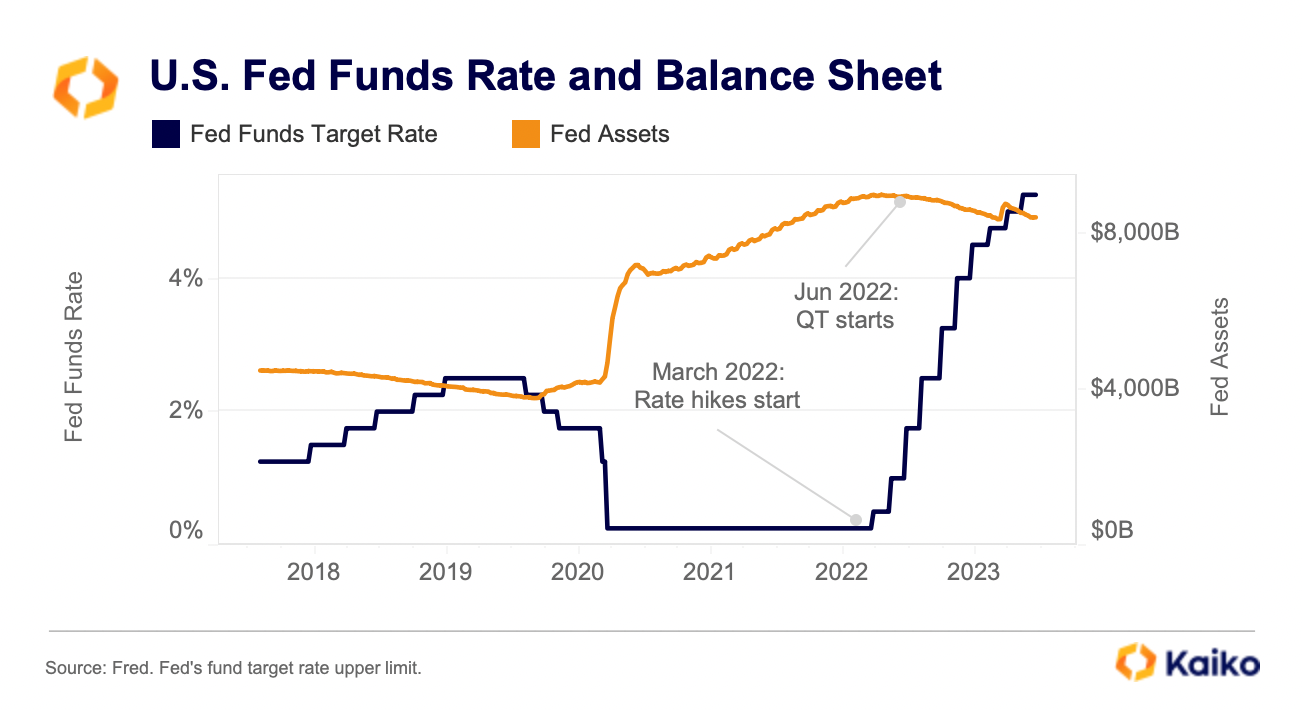

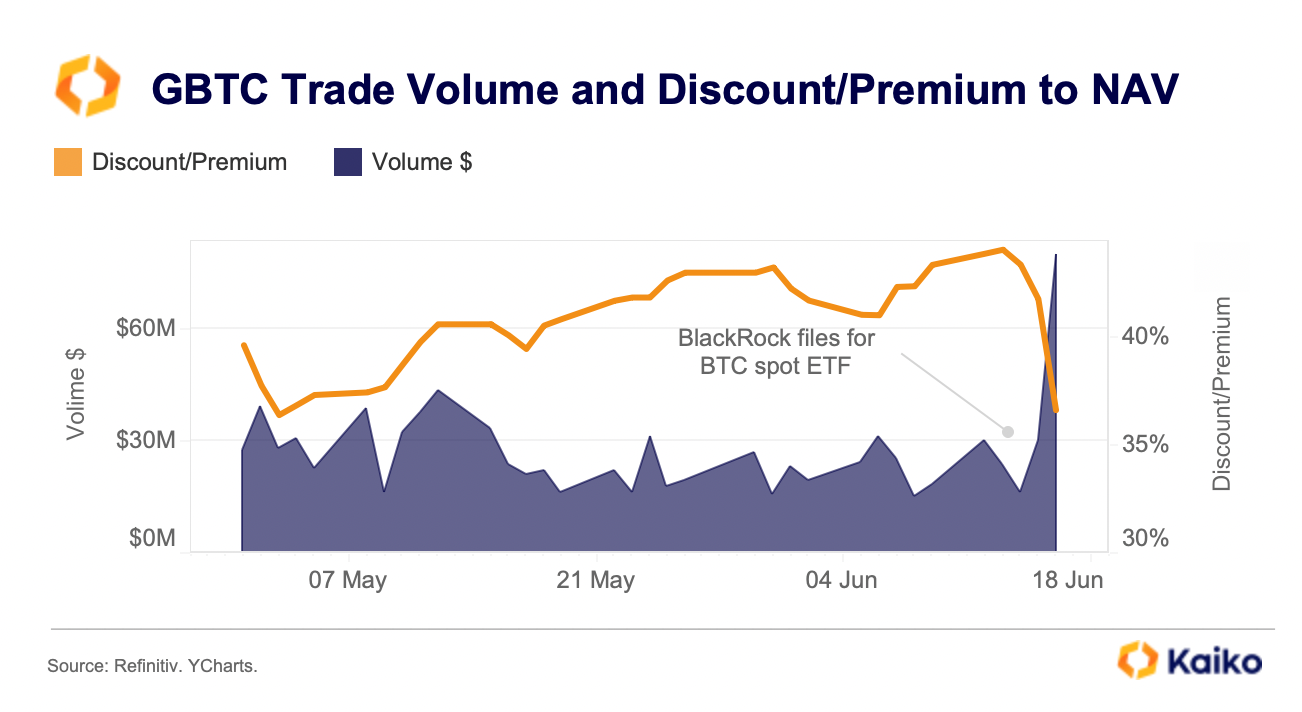

Crypto markets made slight gains this week after the Fed decided to pause interest rate increases, a bullish signal for risk assets, and Blackrock filed for a spot bitcoin ETF, a surprise move amid a tough U.S. regulatory environment. This week, we explore:

Data Used in this Analysis

Derivatives Metrics

Metrics and analytics products tailored to the cryptocurrency derivatives market.

Liquidity Metrics

The most granular order book data in the industry optimized for quantitative analyis.

Trade Volume

Centralized exchange data sourced from the most liquid venues, covering all traded instruments.

More data blogs from kaiko

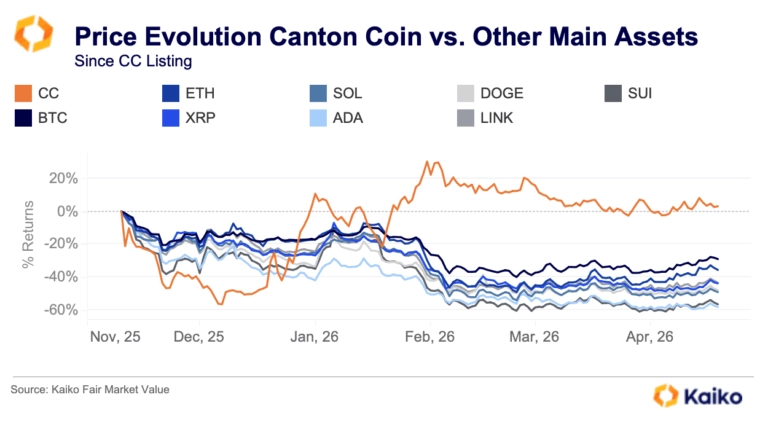

![]() Index in Focus: Inside Out Canton, Ecosystem And Coin

Index in Focus: Inside Out Canton, Ecosystem And Coin07/05/2026

Data Blog21shares, one of the world’s leading issuers of crypto exchange-traded funds (ETFs), announced the launch of

the 21shares Canton Network ETF (Ticker: TCAN). The fund is the first U.S. ETF designed to offer investors

direct exposure to the Canton Coin (CC), the native utility token of the Canton Network.![]() BTC Unfazed by Billion Dollar Sale

BTC Unfazed by Billion Dollar Sale28/07/2025

Data BlogIt’s a big week ahead for macro news, with multiple central bank meetings, including the Fed, and a plethora of economic data to sift through. Moreover, crypto markets just absorbed a enormous $9bn BTC sale without much fuss. We explore all these topics and more in this week’s debrief.

![]() Gap Grows Between Bitcoin and Altcoins

Gap Grows Between Bitcoin and Altcoins07/07/2025

Data BlogBitcoin came close to a new all-time high last week before strong U.S. jobs data dented rate-cut hopes and pulled markets lower. Yet momentum remains intact, driven by institutional demand and a clear shift toward Bitcoin over altcoins. This week, we explored the structural shifts that may be laying the groundwork for a breakout.